Calculating the indirect cost rate percentage is crucial for organizations, particularly those engaging in federal contracts or grants where demonstrating cost efficiency is essential. Indirect costs, unlike direct costs which can be traced directly to specific projects or activities, are costs that benefit more than one project or department within an organization. These might include utilities, administrative staff, or maintenance. Understanding and applying a correct Indirect Cost Rate Percentage (ICR%) helps in pricing projects accurately, ensuring financial sustainability, and complying with grant or contract requirements. Here are five simple Excel formulas you can use to calculate your indirect cost rate percentage effectively.

1. Basic Indirect Cost Rate Percentage Calculation

The simplest formula to start with is the basic calculation of the ICR%, which can be expressed in Excel as:

=INDIRECT COSTS / (DIRECT COSTS + INDIRECT COSTS)

- Indirect Costs: These are costs not directly attributable to a specific project.

- Direct Costs: Costs directly associated with producing goods or services for a project.

2. Calculating Modified Total Direct Cost (MTDC)

In some cases, particularly in federal funding, a specific subset of direct costs called Modified Total Direct Cost (MTDC) is used. Here’s how you can calculate it:

=SUM(DIRECT COSTS) - EXCLUDED COSTS

- Excluded costs can include items like capital expenditures, equipment, alterations and renovations, etc., which are defined by the funding agency.

⚠️ Note: Always refer to specific agency regulations for what can be excluded from MTDC calculations.

3. Using a Cap on Indirect Cost Rate

Funding agencies might impose a cap on the indirect cost rate that can be charged. Here’s a formula to apply this:

=IF(INDIRECT COSTS/DIRECT COSTS > CAP RATE, CAP RATE, INDIRECT COSTS/DIRECT COSTS)

- Where CAP RATE is the maximum indirect cost rate allowed by the funding agency.

4. Calculating Provisional Rates

A provisional rate might be set when the exact figures for indirect costs aren’t known yet. This rate could be adjusted later based on actual figures. Here’s a simple formula:

=PROVISIONAL RATE * DIRECT COSTS

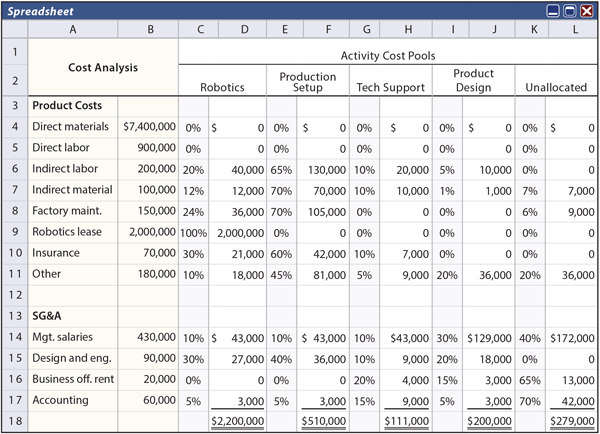

5. Indirect Cost Allocation Based on Cost Pool

Organizations might use cost pools to allocate indirect costs. Here’s how you can do this in Excel:

=COST POOL BASE / (SUM OF ALLOCATION BASE FOR ALL POOLS * (INDIRECT COSTS/SUM OF ALL COSTS))

| Cost Pool | Allocation Base | Pooled Costs | Rate |

|---|---|---|---|

| Personnel | Direct Labor Hours | 100,000</td> <td>=C2/SUM(B2:B5)</td> </tr> <tr> <td>Equipment</td> <td>Equipment Usage</td> <td>20,000 | =C3/SUM(B2:B5) |

| Office | Office Space | 30,000</td> <td>=C4/SUM(B2:B5)</td> </tr> <tr> <td>Admin</td> <td>Headcount</td> <td>50,000 | =C5/SUM(B2:B5) |

📊 Note: The rates in the above example are illustrative. Ensure all figures are accurate when using these formulas in practice.

Understanding and correctly calculating the indirect cost rate percentage is fundamental for managing organizational finances efficiently. Whether you're dealing with basic calculations, applying caps, or allocating costs through pools, Excel provides a straightforward and powerful tool to perform these tasks. By using the formulas outlined above, organizations can better manage their costs, align with regulatory requirements, and make strategic decisions that contribute to their financial health.

What exactly are indirect costs?

+Indirect costs are expenses that cannot be easily identified with a specific project or activity. Examples include administrative salaries, utilities, and office supplies that benefit more than one project.

Why is a cap on indirect costs important?

+A cap on indirect costs ensures that organizations do not overcharge or profit excessively from indirect costs. It’s particularly relevant in government contracts or grants to prevent financial mismanagement.

How often should the indirect cost rate be recalculated?

+The frequency of recalculating indirect cost rates can depend on regulatory requirements or internal policy, but generally, it’s reviewed annually or when significant changes in cost structures occur.

Can indirect costs be included in grant applications?

+Yes, but often with limitations or specific conditions. Indirect costs must be justifiable and typically capped by the funding agency’s regulations.

What is the purpose of using a cost pool for indirect costs?

+Using a cost pool helps organizations distribute indirect costs equitably across different projects or departments based on usage or benefit received, ensuring a more accurate cost allocation.